Nvidia Q1 Results Beat Wall Street: Is It Too Late to Buy the AI Super-Stock in May 2026?

The undisputed king of the artificial intelligence hardware boom has done it again. On Wednesday, May 20, 2026, Nvidia Corporation dropped its highly anticipated Q1 fiscal 2027 earnings report, delivering a masterclass in market dominance that left Wall Street analysts scrambling to rewrite their valuation models. Heading into the print, critics repeatedly warned that the tech giant’s growth curve had peaked, suggesting that any minor earnings hiccup would trigger a massive tech stock sell-off.

Instead, Santa Clara responded with an absolute structural blowout.

Driven by uncompromised global demand for its high-end graphic processing architectures, the firm completely cleared Wall Street’s consensus projections across every major financial line. Following the report, Nvidia’s stock experienced a typical, short-term post-earnings slip of roughly 1.5% in after-hours trading—a familiar “sell-the-news” pattern that has historically served as a temporary pause before another massive upward run.

With the stock hovering around a historic $5.4 trillion market valuation, investors face a critical question during this Nvidia Q1 Earnings May 2026 cycle: Is it too late to buy into the AI super-stock, or is the generative intelligence hypercycle just entering its most profitable phase? Let’s break down the hard numbers, the structural shifts, and the capital metrics defining the company today.

1. Deconstructing the Q1 Blowout: The Numbers You Need to Know

Nvidia did not just beat analyst expectations; it systematically outpaced them, proving that the corporate buildup of “AI factories” is accelerating with immense momentum.

The Core Ledger Breakdown:

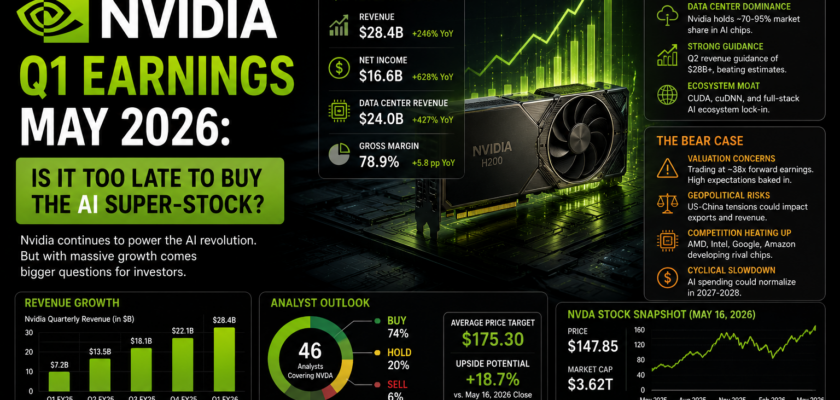

- Total Revenue: Surged to a record-breaking $81.6 billion, marking an exceptional 85% increase year-on-year and clearing the Street’s consensus estimate of $78.8 billion by a massive $2.8 billion margin.

- The Data Center Engine: Revenue within the core Data Center division climbed to a staggering $75.2 billion, up 92% from a year ago, fueled directly by massive hardware deployments across the cloud landscape.

- Pricing Power Security: The firm’s non-GAAP gross margins held incredibly steady at a highly profitable 75%, proving that the company maintains absolute control over its pricing structures even as its next-gen Blackwell hardware architecture enters full production.

- The Next Horizon Guidance: Looking ahead, Nvidia issued a blockbuster Q2 revenue guidance of $91.0 billion (plus or minus 2%), entirely eclipsing the $86.8 billion framework that conservative analysts had penciled in.

[ Nvidia Q1 FY2027 Financial Snapshot ]

│

┌───────────────────────────┴───────────────────────────┐

▼ ▼

┌─────────────────────────────────┐ ┌─────────────────────────────────┐

│ Reported Revenue Lines │ │ Capital Return Parameters │

│ • Total Revenue: $81.6B (+85%) │ │ • Quarterly Dividend: $0.25 │

│ • Data Center: $75.2B (+92%) │ │ (A massive 25-fold increase) │

│ • Q2 Revenue Guide: $91.0B │ │ • Fresh Buyback: $80 Billion │

└─────────────────────────────────┘ └─────────────────────────────────┘

2. The Buried Story: The 25x Dividend Jump and Buyback Surge

While headline revenues captured the primary media attention, the most profound transformation within the Nvidia Q1 Earnings May 2026 report lies in its capital allocation shifts. Nvidia is rapidly transitioning from a pure high-growth tech play into an absolute cash-generating machine.

The company’s board of directors approved a massive 25-fold increase in its quarterly cash dividend, bumping the payout from a nominal $0.01 per share to $0.25 per share. Simultaneously, the board authorized an additional $80 billion share repurchase program on top of the $38.5 billion already remaining in its existing treasury reserves.

During Q1 alone, Nvidia returned a staggering $20 billion to shareholders in the form of buybacks and cash dividends. Pure-growth startups operating on thin margins do not hand back $20 billion to investors in a single quarter; they only do so when their structural free cash flow—which hit $48.6 billion this quarter—is accelerating at an un-bottlenecked velocity.

3. Strategic Matrix: Traditional High-Growth Tech vs. 2026 Nvidia Realities

| Financial Axis | Standard High-Growth Tech Profile | Nvidia Corporation Post-Q1 Realities (2026) |

| Revenue Velocity | Cyclical; vulnerable to sharp post-hype cooling | Highly structural; 85% YoY growth at absolute scale |

| Gross Margin Profile | Compressing as manufacturing and supply lines scale | Immaculate 75% baseline; zero pricing degradation |

| Shareholder Returns | Minimal dividends; heavy reliance on equity prints | Aggressive capital return (25x dividend hike + $80B buyback) |

| Revenue Guidance | Conservative; impacted by regional market cooling | Bullish $91.0B guide; completely excludes China lines |

| Investment Profile | High speculation; volatile tailwind assumptions | Minimized Risk; foundational infrastructure monopolization |

4. The Long View: Is It Too Late to Buy NVDA?

For individual retail investors and large-scale asset managers tracking long-term capital preservation, the post-earnings environment presents an attractive point of entry rather than a late-stage risk. The “AI Bubble” narrative fails when contrasted against the hard reality of hyperscaler balance sheets.

Major technology conglomerates are collectively on track to spend over $725 billion in combined capital infrastructure layout during 2026 alone. Because Nvidia’s proprietary CUDA software layer acts as a digital moat, it remains nearly impossible for competitive chip firms to easily displace their ecosystem.

Furthermore, consider the sheer scale of the upcoming hardware horizon: the company’s Q2 guidance of $91 billion was achieved with zero data center compute revenues coming out of China, providing a massive layer of insulation from international geopolitical friction. As the company safely maneuvers through its annual product lifecycle—gradually transitioning from Hopper configurations to full-scale Blackwell deployments before building out its next-gen Vera Rubin tracks—demand continues to outpace production capacities across the globe.

Conclusion

We have graduated from the era of speculative AI hype. The widespread clarity delivered by the latest financial results proves that computing infrastructure is the most valuable and foundational commodity of the modern digital economy.

Chasing short-term day-trading ticks within the daily abacus maze is an operational liability that frequently leads to missed opportunities. While a $5.4 trillion price tag can induce natural valuation anxiety, the company’s accelerating free cash flows, staggering 25x dividend expansion, and dominant market position indicate that the stock’s forward runway remains completely uncompromised.

It is not too late to buy the defining asset of the decade. By treating any temporary post-earnings consolidation as a high-yield accumulation zone, investors are aligning themselves with the core processing factory of the future. The machines require silicon to think—and as long as that biological reality holds, Nvidia remains the absolute gatekeeper of the global technology current.