India Money Market Volumes: Why the ₹7 Lakh Crore Mark Matters

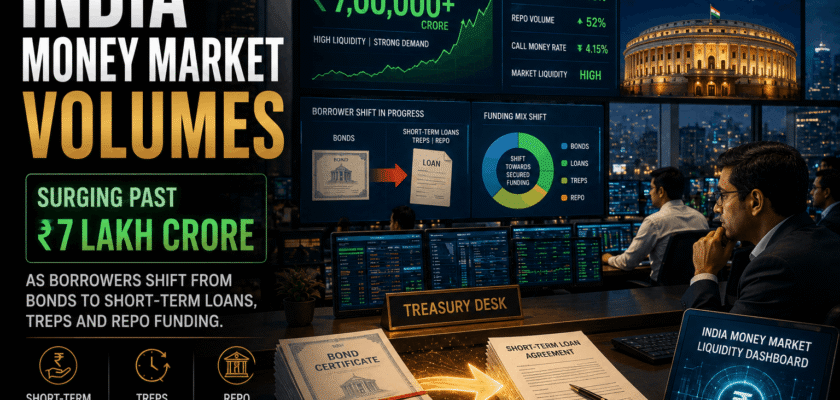

India money market volumes have become a major finance story because short-term funding activity is moving through India’s overnight and repo markets at record scale. Market trackers reported that the overnight money market segment crossed roughly ₹7.63 lakh crore on June 1, 2026, with activity concentrated in TREPS, market repo, call money and related secured funding channels. That is a huge liquidity signal for banks, mutual funds, corporates and treasury desks.

This surge is not only a technical market event. It shows how Indian borrowers and lenders are adjusting to a high-uncertainty environment where the Reserve Bank of India has kept the repo rate steady at 5.25%, the rupee has faced pressure, oil prices have stayed sensitive to West Asia risk and investors are watching the shift between bond issuance, bank loans and short-term money market funding.

In simple words, India money market volumes are rising because institutions want fast, liquid, low-tenure funding routes when long-term borrowing looks uncertain or costly.

Why India Money Market Volumes Matter in 2026

India money market volumes matter because they show the real-time demand for short-term liquidity. When money markets become busy, it means banks, corporates, mutual funds and financial institutions are actively parking, borrowing and managing cash for very short periods.

Reuters reported that on June 5, 2026, RBI kept the repo rate unchanged at 5.25% and focused on currency-stability measures instead of raising rates, even though rupee weakness, oil prices and the Iran conflict were adding inflation risk. This stable repo backdrop helped overnight rates stay anchored near the policy rate.

A stable policy rate supports money market activity because participants can price overnight and short-term funds with more confidence. If rate expectations were suddenly unstable, treasury desks would become more cautious.

For the broader economy, strong money market volumes can indicate better liquidity transmission, more active collateral use and stronger short-term funding channels.

What Is the Money Market?

The money market is the part of the financial system where institutions borrow and lend money for short periods. These periods can be overnight, a few days, a few weeks or up to one year depending on the instrument.

It is different from the bond market, where borrowing is usually longer term. It is also different from the equity market, where investors buy ownership in companies.

India’s money market includes instruments such as:

- Call money

- Notice money

- Term money

- Triparty repo, also called TREPS

- Market repo

- Repo in corporate bonds

- Commercial paper

- Certificates of deposit

- Treasury bills

- Short-term bank and corporate funding products

The Reserve Bank of India explains that TREPS is an anonymous order-matching system that allows members to borrow and lend funds through triparty repo deals, with online dissemination of deals, volumes and rates.

What Does “Shifting from Bonds to Loans” Mean?

Shifting from bonds to loans means borrowers may choose shorter-tenure or relationship-based funding instead of issuing longer-term bonds. This can happen when bond yields are volatile, investor appetite is uneven or companies want flexible funding rather than locking into longer debt.

In the current environment, some borrowers may prefer loans, repo funding, commercial paper or short-term treasury routes because they can manage cash more actively. Lenders may also prefer secured short-term funding where collateral and liquidity are clearer.

This does not mean bonds are disappearing. India still needs a deeper corporate bond market. It means that in a volatile phase, the balance between bonds, bank loans and money market instruments can shift.

Why Volumes Surged Past ₹7 Lakh Crore

The reported surge past ₹7 lakh crore reflects a mix of liquidity management, secured funding demand and active treasury participation. Market reports put the overnight segment at about ₹7.63 lakh crore on June 1, 2026, including large TREPS and market repo activity.

Several factors can explain this jump:

- RBI repo rate stability near 5.25%

- High demand for short-term liquidity

- Active mutual fund and bank treasury participation

- Preference for secured funding routes

- Rupee and oil-price uncertainty

- Need to park surplus cash efficiently

- Borrowers avoiding long-term rate risk

- Growth in triparty repo infrastructure

- Better collateral-based market participation

- More institutional use of overnight funding channels

The key point is that money market volumes do not rise only because one segment is hot. They rise when multiple participants use short-term funding channels at the same time.

TREPS: The Biggest Driver of Short-Term Volumes

TREPS, or triparty repo, is one of the most important parts of India’s short-term funding market. In a triparty repo, a borrower raises funds against eligible securities, and a third-party platform helps manage settlement and collateral.

NSE explains that the aim of introducing triparty repo was to improve liquidity in the corporate bond repo market and provide an alternative to government securities repo. This is important because it expands secured borrowing and lending options.

TREPS is attractive because it offers:

- Secured lending structure

- Collateral-based comfort

- Efficient settlement

- Short-term flexibility

- Large institutional participation

- Useful cash parking route

- Transparent platform-based dealing

- Better liquidity for treasury desks

- Alternatives to unsecured lending

- Operational ease

When TREPS volumes rise, it usually means institutions are using secured money market routes actively rather than keeping idle liquidity unproductive.

Market Repo: Why Secured Funding Is Preferred

Market repo is another important secured funding route. In a repo transaction, one party sells securities with an agreement to repurchase them later. Economically, it works like borrowing against securities.

In uncertain markets, secured funding becomes attractive because lenders have collateral protection. Borrowers also get short-term cash without selling securities permanently.

Market repo supports:

- Bank liquidity management

- Treasury operations

- Collateral utilization

- Short-term funding

- Repo-rate transmission

- Money market depth

- Institutional cash movement

- Risk-managed lending

- Funding flexibility

- Efficient settlement

This is why repo markets often become very active when institutions want quick and safer funding routes.

Call Money and Notice Money

Call money is overnight borrowing and lending, mainly between banks and eligible institutions. Notice money is for short periods beyond overnight, usually 2 to 14 days. These markets help banks manage daily liquidity gaps.

Reuters reported in April 2026 that RBI opened the term money market to non-bank companies to boost participation. It noted that daily average volumes in term money were much smaller than notice money and overnight call money, which shows how dominant short-end liquidity remains in India.

This matters because deeper term money participation could eventually reduce pressure on overnight markets. But for now, India’s short-term liquidity activity remains heavily concentrated in overnight and repo-linked instruments.

Commercial Paper and Certificates of Deposit

Commercial paper, or CP, is a short-term unsecured debt instrument usually issued by companies, NBFCs and financial institutions. Certificates of deposit, or CDs, are short-term instruments issued by banks to raise funds.

When companies shift from longer bonds to shorter borrowing, CP can become useful. But CP is unsecured, so investors carefully watch issuer quality, ratings, liquidity and market sentiment.

CDs help banks raise short-term funds, especially when deposit growth, credit growth and liquidity conditions need balancing.

Together, CP and CD markets show how companies and banks manage short-term funding needs outside traditional long-term borrowing.

RBI Repo Rate Stability and Money Market Pricing

The RBI repo rate is the anchor for short-term money market pricing. When the repo rate is stable, overnight rates usually trade near the policy corridor unless liquidity becomes very tight or very loose.

On June 5, 2026, RBI kept the repo rate at 5.25%. Reuters reported that the central bank avoided rate hikes while announcing measures to attract inflows and defend the rupee.

This matters because short-term money market rates often reflect policy-rate expectations more quickly than long-term bond yields. When RBI pauses, treasury desks can price overnight borrowing and lending with a clearer reference point.

Why Bonds May Look Less Attractive in Volatile Phases

Bonds are useful for long-term financing, but they can become difficult when yields are volatile. If investors demand higher yields, companies may delay issuance or look for bank loans and short-term funding instead.

Borrowers may avoid long bonds when:

- Interest-rate outlook is unclear

- Credit spreads are widening

- Investor demand is weak

- Rupee volatility is high

- Oil price risk increases inflation fear

- Long-term borrowing cost looks expensive

- Debt market liquidity is uneven

- Company cash needs are temporary

- Banks offer competitive loan terms

- Management wants funding flexibility

This is why the phrase shifting from bonds to loans makes sense in a volatile phase. It is about funding flexibility.

Why Loans Can Look More Practical

Loans can look more practical because they are relationship-based and can be negotiated directly with banks or lenders. For some companies, a short-term loan or working capital line is easier than going to the bond market.

Loans can offer:

- Faster access to funds

- Flexible repayment structures

- Relationship banking support

- Working capital fit

- Less market timing risk

- Better customization

- Bridge funding option

- Credit line availability

- Easier refinancing for some borrowers

- Bank-led monitoring

However, loans are not always cheaper. They may carry covenants, collateral requirements, spread resets and bank-specific terms. Companies must compare total cost, flexibility and refinancing risk.

Money Market Volumes and Corporate Treasury Strategy

Corporate treasuries use money markets to manage daily cash needs. A company may have surplus cash for a few days, or it may need short-term funding before receivables arrive. Money markets help solve these timing gaps.

A good treasury desk uses money market instruments for:

- Cash parking

- Working capital timing

- Short-term borrowing

- Liquidity buffers

- Rate-risk management

- Debt maturity planning

- Collateral planning

- Bank relationship management

- Investment of surplus funds

- Emergency liquidity access

When India money market volumes rise sharply, it shows that treasury activity is becoming more intense and sophisticated.

Why Mutual Funds Matter in Money Markets

Liquid funds and money market funds are major participants in short-term instruments. They park investor money in safe, short-duration instruments and help channel surplus liquidity into the financial system.

If corporates and institutions start participating more directly in money markets, it can affect how money moves through liquid mutual funds. Reuters noted in April 2026 that direct corporate and NBFC participation in term money could affect liquid mutual fund schemes because many corporates currently park excess cash there.

This is important because money market structure affects mutual fund flows, bank liquidity and short-term rates.

Rupee Defence Measures and Market Liquidity

RBI’s June 2026 policy was not only about repo rate. It also included currency support measures. Reuters reported that RBI and the government announced steps such as concessional forex swaps, support for FCNR(B) deposits and expanded access for foreign investors to Indian government bonds.

These measures aim to attract dollar inflows and stabilize the rupee. When currency pressure is high, domestic liquidity and money market confidence also become important.

If the rupee stabilizes, foreign investors may become more comfortable with Indian debt. If the rupee weakens sharply, funding conditions can tighten.

Foreign Bond Investors and the Tax Exemption Signal

Reuters reported that the Indian government announced exemptions from capital gains tax on interest and sales of government securities for foreign investors as part of broader measures to support inflows. This is relevant because foreign bond participation can affect domestic bond yields and liquidity.

If foreign demand for government bonds improves, it can support the bond market. But if companies still see better flexibility in loans or short-term markets, the shift toward money market funding can continue in selected segments.

This shows how policy measures affect both bond markets and short-term funding channels.

Why the ₹7 Lakh Crore Figure Is a Liquidity Signal

The ₹7 lakh crore figure should be read as a liquidity signal, not as a simple “good or bad” number. High volumes mean the market is active, but analysts must check whether the activity is healthy or driven by stress.

Healthy volume means:

- Active cash management

- Good market depth

- Efficient repo settlement

- Strong institutional participation

- Stable overnight rates

Stress volume may mean:

- Funding pressure

- Liquidity hoarding

- Rate volatility

- Collateral scarcity

- Risk aversion

So, the important question is not only how big the volume is. The important question is whether rates remain orderly and participants keep confidence.

Impact on Banks

Banks are central to money market activity. They borrow, lend, manage reserve requirements, fund loan growth and invest in short-term instruments.

Rising money market activity can help banks:

- Manage daily liquidity

- Price short-term funds efficiently

- Support lending books

- Use securities as collateral

- Respond to deposit gaps

- Balance treasury positions

- Reduce idle funds

- Improve market participation

- Manage RBI policy transmission

- Support interbank stability

However, if funding stress rises, banks may become cautious and loan pricing can tighten.

Impact on Corporates

Corporates benefit from a deep money market because it gives them alternatives to long-term bonds and bank-only borrowing. A company can choose the funding route that best matches its need.

Corporate benefits include:

- Short-term working capital funding

- Cash parking options

- Lower dependency on long bonds

- More treasury flexibility

- Better liquidity management

- Funding diversification

- Temporary bridge finance

- Access to CP markets if rated well

- Efficient use of surplus cash

- Better rate comparison

But corporates must also manage rollover risk. Short-term borrowing must be refinanced frequently.

Impact on NBFCs

NBFCs are sensitive to funding costs because they borrow from markets and lend to customers. If money markets remain deep and stable, NBFCs can manage short-term liquidity more confidently.

But NBFCs must be careful because heavy short-term borrowing can create maturity mismatch. If market conditions change quickly, refinancing can become difficult.

A strong NBFC funding strategy balances:

- Bank loans

- Debentures

- Commercial paper

- Securitization

- Term borrowing

- Capital buffers

- Liquidity coverage

- Asset-liability matching

- Investor confidence

- Credit ratings

Impact on Investors

Retail investors usually do not directly trade in institutional money markets, but they are affected indirectly through liquid funds, short-duration funds, bank deposit rates, bond yields and credit availability.

Investors should watch:

- Liquid fund yields

- Short-duration debt fund returns

- Credit risk in CP holdings

- Bank CD rates

- RBI repo rate stance

- Rupee movement

- Government bond yields

- Corporate bond spreads

- Oil prices

- Liquidity conditions

Money market strength can support stable returns in low-duration debt categories, but investors should still check portfolio quality and maturity profile.

Why Short-Term Debt Funds May Get Attention

When money market volumes rise and rates stay near policy levels, short-term debt funds may attract investors seeking lower volatility than equities. However, debt funds are not risk-free.

Investors should check:

- Portfolio credit quality

- Average maturity

- Modified duration

- Expense ratio

- Exit load

- Yield-to-maturity

- Issuer concentration

- Fund house quality

- Liquidity profile

- Past risk events

A high yield in a debt fund may signal higher credit risk. Safety matters more than chasing extra return.

Why Corporate Bond Market Still Needs Deepening

The shift toward money markets does not remove the need for a strong corporate bond market. India still needs deeper long-term financing channels for infrastructure, manufacturing, energy, real estate, logistics and private investment.

A deep corporate bond market helps:

- Long-term funding

- Infrastructure finance

- Investor diversification

- Reduced bank dependence

- Better credit pricing

- Pension and insurance investment

- Stable capital formation

- Alternative to bank loans

- Transparent debt markets

- Financial system resilience

Money markets solve short-term needs. Corporate bonds solve long-term funding needs. India needs both.

Risk 1: Rollover Risk

Rollover risk is the risk that a borrower cannot refinance short-term debt when it matures. This is a key risk when companies depend heavily on short-tenure funding.

If market conditions tighten suddenly, a company may face higher rates or funding difficulty. This is why short-term money market borrowing should match short-term needs, not long-term projects.

Risk 2: Liquidity Stress

High money market volumes are healthy only if liquidity remains orderly. If participants start hoarding liquidity or rates spike, the same market can become a stress point.

RBI monitors money market rates, liquidity absorption, liquidity injection, repo operations and system liquidity to keep markets stable.

Risk 3: Credit Quality

Instruments such as commercial paper depend heavily on issuer quality. If a company’s credit profile weakens, refinancing CP can become difficult.

Investors and treasuries should not treat all money market instruments as equal. Government-backed, bank-backed and high-rated corporate instruments carry different risk levels.

Risk 4: Interest Rate Uncertainty

RBI held the repo rate at 5.25% on June 5, 2026, but Reuters reported that the central bank signalled a watchful approach and possible tightening later if conditions worsen. That means short-term rates can still move if inflation, rupee weakness or oil shock intensifies.

Borrowers should not assume rates will remain unchanged forever. They should build buffers.

What CFOs Should Do Now

CFOs should use the current money market activity to review their funding mix. The goal is not to blindly shift from bonds to loans, but to match funding with business need.

CFOs should:

- Map debt maturities for the next 12 months

- Compare bank loan rates with CP and bond yields

- Avoid using short-term debt for long-term assets

- Maintain liquidity buffers

- Diversify lenders and investors

- Track repo and TREPS rates

- Review FX exposure if imports are high

- Stress-test refinancing risk

- Keep board-level funding policy clear

- Prepare backup credit lines

What Investors Should Watch Next

Investors should watch whether high money market volumes continue and whether rates remain close to the policy corridor. They should also track RBI liquidity operations and rupee movement.

Key signals include:

- TREPS daily volumes

- Market repo volumes

- Weighted average call rate

- RBI repo rate stance

- Government bond yields

- Corporate bond spreads

- CP and CD issuance

- Rupee-dollar movement

- Foreign portfolio flows

- Oil price direction

If volumes stay high with stable rates, that signals healthy liquidity depth. If rates jump, that signals pressure.

What Retail Readers Should Understand

Retail readers do not need to trade money markets directly to understand the story. The message is simple: India’s financial system is using short-term markets very actively to manage liquidity in a volatile phase.

This affects the wider economy through:

- Loan pricing

- Bank liquidity

- Debt fund returns

- Corporate borrowing cost

- Bond market sentiment

- Currency stability

- Investor confidence

- Working capital availability

- NBFC funding cost

- Financial-market stability

So, a ₹7 lakh crore money market volume headline is not just for bankers. It affects the cost and availability of money across the economy.

Final Verdict

India money market volumes crossing the ₹7 lakh crore mark shows how active short-term funding has become in 2026. The surge reflects liquidity management, secured repo activity, TREPS growth, RBI repo-rate stability and borrower preference for flexible funding routes in a volatile macro environment.

The shift from bonds to loans does not mean India is abandoning bond markets. It means companies and institutions are using different funding tools depending on cost, flexibility, maturity and risk. In uncertain conditions, short-term loans, repo routes and money market instruments can look more practical than long-term bond issuance.

In simple words, India’s money market is becoming the financial system’s pressure valve. It helps banks, corporates, NBFCs and investors move cash quickly when the economy faces oil shocks, rupee pressure and rate uncertainty.

The opportunity is clear: deeper money markets can improve financial flexibility. The warning is also clear: short-term funding must be used responsibly because rollover risk, credit risk and liquidity stress can rise quickly.

For India, the best path is not bonds versus loans. It is a balanced financial system where money markets, bank loans and corporate bonds all grow together.