{kind=link}

The Fed’s Reserve Management Move: How the New Policy Aims to Protect Portfolios from Stagflation.

The foundational core of global monetary policy has shifted into a highly defensive posture. For the past several quarters, institutional asset managers and private investors operated under a relatively predictable macroeconomic assumption: that central bank interventions would follow a standard, cyclical loop. When economic growth surged, the central bank raised borrowing costs to cool demand; when recession risks appeared, they promptly cut interest rates to flood the system with liquidity. It was an established framework designed for a world where inflation and economic growth generally moved in the same direction.

But as we advance through late May 2026, that legacy monetary framework has run straight into a wall.

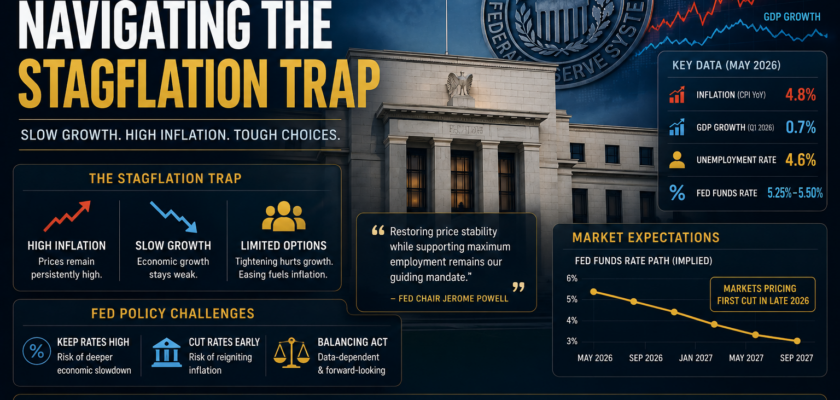

The complex supply shock triggered by the West Asia war and the prolonged blockade of the critical Strait of Hormuz has forced consumer price index (CPI) markers up past 3.8%, driving an abrupt upward shift in the global inflation regime. Concurrently, manufacturing gauges are signaling clear signs of slowing industrial growth and narrowing corporate profit margins.

Faced with this classic, high-risk stagflation trap—characterized by high inflation and stalling economic growth occurring simultaneously—the old policy levers are officially jammed.

Recognizing that traditional interest rate cuts risk feeding the inflation fire while aggressive rate hikes could plunge the economy into a deep recession, the central bank has executed a historic pivot.

The newly announced US Federal Reserve policy May 2026 directives mark a profound structural evolution. Following the historic leadership transition on Friday, May 15, 2026, which saw Jerome Powell step down and new Fed Chair Kevin Warsh assume the helm, the central bank is completely overhauling its reserve management guidelines. This fresh architecture aims to systematically protect multi-asset portfolios, decouple structural liquidity from energy shocks, and build a non-inflationary buffer for the modern economy.

1. The Stagflation Crucible: Why the Old Monetary Playbook Failed

To understand why a sweeping overhaul of reserve management was necessary, one must analyze the biological mechanics of a stagflationary environment. Under a normal economic contraction, dropping interest rates is a safe, highly effective way to stimulate consumer spending because high supply and low demand keep core prices naturally suppressed.

[ The Standard Cyclical Loop ]

(Economic Slack ──► Interest Rate Cuts ──► Non-Inflationary Growth Rescue)

│

▼

[ The 2026 Stagflation Trap ]

(Supply-Driven Inflation + Slowing GDP ──► Traditional Rate Cut = Hyper-Inflation)

│

┌───────────────────────────┴────────────────___________┐

▼ ▼

┌─────────────────────────────────┐ ┌─────────────────────────────────┐

│ The Supply-Shock Reality │ │ The Margin Compression Squeeze│

│ • Energy costs drain household cash│ │ • Input costs rise faster than sales│

│ • Real wages experience drops │ │ • Corporate layoffs accelerate │

│ • Pushes top-line CPI past 4% │ │ • Standard rate tools lose grip │

└─────────────────────────────────┘ └─────────────────────────────────┘

The 2026 supply shock breaks this dynamic entirely. Because current price increases are driven by external bottlenecks—such as soaring transport costs and sky-high global energy assets rather than excess consumer demand—slashing interest rates would merely lower the purchasing power of the dollar without adding a single new barrel of oil to the market.

- The Squeeze on Consumers: Higher energy costs are acting as a permanent “crisis tax” on global households, consuming up to 5% of average budgets and directly weakening general domestic consumption.

- The Threat of Real Wage Drops: As nominal wage growth falls behind top-line inflation markers, consumers face a sharp drop in real purchasing power. This shift triggers sudden drops in consumer sentiment and slows down retail economic velocity.

- The Double-Sided Policy Risk: Central banking leadership acknowledges that using old-school, aggressive demand-side tightening to fight supply-side inflation risks crushing an already fragile job market. This reality demands a brand-new approach to managing systemic liquidity.

2. Re-Engineering Liquidity: The Core Pillars of the New Reserve Policy

Rather than treating the federal funds rate as the sole mechanism to steer the economy, the new Fed leadership under Kevin Warsh is deploying a sophisticated series of structural balance sheet and payment infrastructure reforms. This approach targets the plumbing of the banking sector to isolate and absorb economic shocks.

A. The Institutionalization of “Payment Accounts”

In a monumental structural shift finalized on Wednesday, May 20, 2026, the Federal Reserve proposed a comprehensive legal framework for specialized “payment accounts” (frequently termed skinny master accounts).

[ Eligible Fintech / Neo-Bank ] ───► [ Direct Federal Reserve Payment Account ]

│

▼

[ Isolated Clearance & Settlement ]

"Direct Rails Access via Fedwire Architecture"

│

▼

[ Non-Inflationary Liquidity Shield ]

"No Discount Window Access, No Interest Accrual"

Designed to accelerate the integration of fintech firms and digital asset innovators directly into the nation’s payment infrastructure, this rule allows eligible non-bank financial institutions to settle payments directly on the Fedwire rail.

Crucially, these specialized accounts feature zero access to the emergency discount window and earn absolutely no interest on balances held at the Fed.

By providing direct settlement infrastructure while intentionally withholding interest accrual on these specific pools, the Fed is clearing out bloated layers of commercial bank intermediation. This structure allows liquidity to circulate rapidly throughout the digital economy without artificially inflating the baseline money supply—creating an elegant, non-inflationary structural cushion.

B. Looking Through Supply Shocks via Macro Guidance

Parallel to this architectural upgrade, the Warsh-led central bank is shifting its public policy communication strategy. Moving away from a rigid focus on backward-looking, headline monthly inflation data, the Board is providing explicit guidance that it intends to “look through” temporary, tariff-driven or oil-induced supply shocks.

By reassuring the markets that the Fed will not execute sudden, knee-jerk interest rate hikes in response to short-term geopolitical events, the policy effectively caps the volatile “fear premium” on the long end of the Treasury curve. This guidance provides a reliable baseline for institutional lending markets to extend capital confidently.

3. Strategic Matrix: Legacy Monetary Frameworks vs. May 2026 Reserve Protections

| Policy Dimension | Legacy Demand-Side Monetary Playbook | May 2026 Fed Reserve Architecture |

| Primary Operational Focus | Aggressive, cyclical manipulation of interest rate bands | Structural payment rails reform & balance sheet design |

| Fintech Systems Stance | Isolated; restricted master account access via bank layers | Integrated; direct “payment account” access rails |

| Supply-Shock Adaptation | Reactive; triggers hawkish tightening or dovish panic | Proactive; explicitly looks through one-off energy spikes |

| Systemic Liquidity Link | Generates high inflationary pressure via interest payments | Non-inflationary; zeros out interest on payment pools |

| Risk Characterization | High vulnerability to sudden policy mistakes and stagflation | Minimized Risk; tech-backed structural insulation |

4. Portfolio Protection: How Investors Can Re-Align Their Assets

For wealth managers, private equity portfolios, and everyday investors navigating this structural shift in how to beat stagflation, the implementation of this new reserve policy requires moving capital away from classic, long-duration growth asset allocations.

[ Extended Central Bank Pause ] ───► [ Multi-Decade Highs in Long-End Yields ]

│

▼

[ High-Utility Allocation Pivot ]

• Lock in high yields on short-to-medium bonds

• Accumulate financially solid, cash-rich equities

• Diversify into emerging market debt assets

│

▼

[ Structural Capital Preservation ]

"Withstands Prolonged Geopolitical Blocks"

With federal funds futures pricing in a high probability that the benchmark rate will remain held steady for an extended period, long-end bond yields are holding firm near historic multi-decade highs. This environment creates a prime window for smart capital to lock in yields.

- The Short-to-Medium Fixed-Income Play: Rather than taking on excessive risk in volatile growth equities, asset managers are parking capital in high-quality corporate and sovereign bonds within the short- and medium-maturity segments. This strategy allows investors to lock in historically high, predictable yields while avoiding the price volatility of longer-duration papers.

- Consolidating Around High-Quality, Cash-Rich Equities: Within equity allocations, investors are actively moving away from highly leveraged, speculative growth firms that depend on ultra-cheap borrowing costs to survive. Portfolios are consolidating around financially solid, cash-rich companies that possess exceptional pricing power and short-duration cash flow cycles. This focus ensures corporate earnings remain highly insulated from rising supply-side input costs.

- Yield-Generating Alternatives: To build an additional buffer against persistent 4% baseline inflation, wealth managers are increasing allocations to diversified equity-income funds, structured covered-call strategies, and select emerging market debt allocations. This approach enhances consistent, recurring cash flows, providing an alternative stream of income that helps preserve real purchasing power even through prolonged international trade blockades.

Conclusion

The sweeping policy transformation unfolding across the US Federal Reserve policy May 2026 updates delivers a permanent, vital lesson to macroeconomists and capital allocators: structural economic challenges cannot be resolved by relying on outdated demand-side monetary formulas. The old abacus maze of trying to manage an complex supply-driven energy crisis by simply raising or lowering baseline interest rates is being replaced by forward-thinking financial design.

By modernizing payment account access, cutting out non-essential commercial banking frictions, and committing to look through temporary geopolitical supply shocks, the new Fed leadership is building a highly resilient financial architecture.

These sophisticated adjustments don’t just shield the banking system from sudden panics; they provide clear, non-inflationary space for the modern digital economy to grow. While navigating an era of persistent energy constraints will continue to demand absolute discipline and rigorous risk management, the structural decoupling of baseline liquidity from external trade blockades offers an extraordinary shield for global portfolios—proving that the ultimate path to economic resilience is built by embracing innovative financial engineering and clear, uncompromised strategic execution.