{kind=link}

Bond Market Yield Curve Adjustments: What Changed

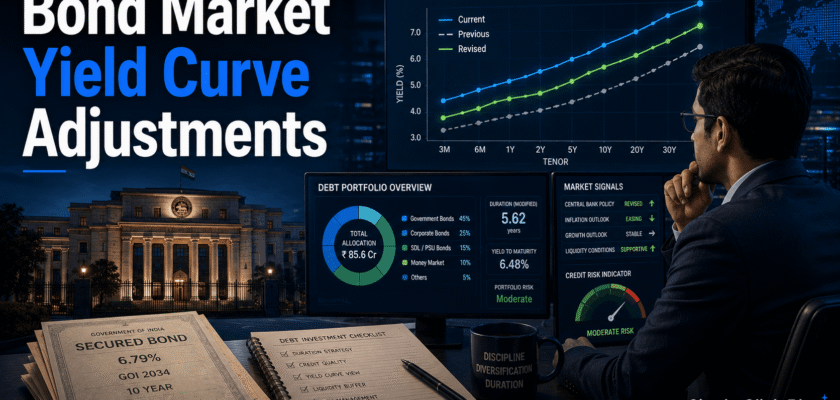

Bond market yield curve adjustments are back in focus for domestic fixed-income investors. Recent RBI-linked measures to support dollar inflows have pushed more attention toward short and medium maturity bonds. As a result, investors are asking whether they should stay short, extend duration or add high-quality corporate debt.

Reuters reported that short-end Indian government bond yields fell after RBI measures encouraged dollar inflows. It also reported that two- to five-year yields dropped by up to 30 basis points, while the five-year and ten-year spread widened.

Meanwhile, companies rushed to issue shorter-tenor debt as borrowing costs softened. Reuters also reported that more than Rs 310 billion in bonds were being raised in one week after borrowing costs fell sharply for some issuers.

Therefore, this is not a normal yield movement. It is a policy-linked curve reset. Investors need a clean plan because the wrong maturity choice can reduce returns when rates, inflation or liquidity conditions shift again.

| KEY TAKEAWAYThe curve is not sending one simple message. Short and medium bonds look more attractive after recent yield moves, but long bonds still carry inflation, currency and global-rate risk. |

Bond Market Yield Curve Adjustments in Simple Words

A yield curve shows the return offered by bonds with different maturities. Usually, longer bonds offer higher yields because investors take more time and inflation risk.

However, the curve changes when central bank policy, liquidity, inflation forecasts or foreign flows change. A small move in policy expectations can change bond prices very quickly.

In the latest setup, short-end yields moved lower faster than long-end yields. Consequently, the curve became steeper. This matters because fixed-income investors earn returns from both coupon income and price movement.

Why Central Bank Revisions Matter for Fixed-Income Investors

Central bank revisions affect the bond market through expectations. When the market believes liquidity will improve, short-tenor bonds often react first. In addition, banks and companies may issue debt faster when funding costs fall.

Recent reports point to RBI steps that encouraged overseas fund-raising, foreign currency deposits and bond inflows. These steps did not only affect the rupee. They also changed demand for short and medium bonds.

At the same time, the repo rate stayed an important anchor. Market reports around the June 2026 policy period described the repo rate at 5.25%, while inflation concerns and global oil risks kept long-end investors careful.

What Domestic Investors Should Watch First

✓ Duration risk: Longer bonds can gain when yields fall, but they can also fall sharply if yields rise.

✓ Reinvestment risk: Very short funds may reinvest at lower yields if rates keep dropping.

✓ Credit risk: Corporate bond spreads can shrink during rallies, but weak issuers remain risky.

✓ Liquidity risk: Some bonds are harder to sell during stress.

✓ Inflation risk: Higher fuel or food prices can change rate expectations.

✓ Currency risk: Foreign inflows can support bonds, but rupee volatility can reverse sentiment.

| INVESTOR SAFETY BOXDo not choose a fund only by past return. Check average maturity, modified duration, portfolio credit quality, expense ratio, exit load and liquidity before investing. |

Strategic Reallocation 1: Keep Core Money in Short to Medium Duration

Short to medium duration funds may suit investors who want better yield capture without taking heavy long-end volatility. This segment has gained attention because recent buying has focused on shorter maturities.

However, investors should still avoid over-concentration. A laddered approach can reduce timing risk. For example, money can be spread across liquid funds, ultra-short funds, short-duration funds and high-quality target maturity options.

Moreover, investors with near-term goals should not stretch duration for small extra yield. Capital stability matters more when the goal is close.

Strategic Reallocation 2: Use Gilt Funds Carefully

Gilt funds invest in government securities. They carry low credit risk, yet they can carry high duration risk. When yields fall, long gilt funds may rise strongly. However, the reverse can also happen.

Because the current curve is policy-sensitive, long gilt exposure should match the investor’s time horizon. Investors with a short goal should not use long gilt funds as a savings account.

Therefore, gilt funds work better as a planned allocation. They are not a guaranteed-return product.

Strategic Reallocation 3: Review Corporate Bond Quality

Corporate bonds may benefit when spreads narrow and issuers borrow at lower cost. Reuters reported that lower borrowing costs encouraged Indian companies to raise short-tenor debt.

Still, credit quality matters. A rally can hide weak balance sheets for a while, but defaults or downgrades can damage returns later.

Consequently, conservative investors should prefer high-quality portfolios, clear issuer diversification and low exposure to complex structured debt.

Strategic Reallocation 4: Build a Maturity Ladder

A maturity ladder spreads money across different time periods. It can reduce the need to guess the exact top or bottom of interest rates.

For example, an investor can keep emergency money in liquid products, one- to three-year goals in short-duration funds and longer goals in carefully selected medium-duration or target maturity funds.

Additionally, a ladder helps manage reinvestment. As one part matures, the investor can reinvest based on the new rate environment.

Where Retail Investors Can Make Mistakes

⚠ Moving all money into long-duration funds after a rally.

⚠ Buying low-rated debt only because the yield looks high.

⚠ Confusing a falling yield with guaranteed future returns.

⚠ Ignoring exit load, taxation and fund expense ratio.

⚠ Using debt funds for emergency money without checking liquidity.

⚠ Following social media tips instead of reading the portfolio factsheet.

How to Read a Debt Fund Factsheet

✓ Average maturity: Shows the weighted maturity of the portfolio. Higher maturity usually means more rate sensitivity.

✓ Modified duration: Shows how much the fund can move when yields change. Higher duration means higher volatility.

✓ Yield to maturity: Shows the portfolio yield before expenses and future changes. It is not a fixed return promise.

✓ Credit rating mix: Shows the quality of issuers. More low-rated debt means more credit risk.

✓ Asset allocation: Shows whether the fund holds government bonds, corporate bonds, money-market papers or cash.

Bond Market Yield Curve Adjustments and Organic Investor Strategy

Bond market yield curve adjustments should lead to a balanced review, not a rushed switch. Investors need to connect each fund choice with a real goal.

For short goals, safety and access should come first. For medium goals, high-quality short or medium-duration products may be useful. For long goals, duration exposure can be added slowly if the investor accepts volatility.

Finally, investors should track inflation, RBI communication, oil prices, rupee movement and global yields. These factors can change the curve again.

Conclusion

Bond market yield curve adjustments have created a new fixed-income decision point. Short and medium maturities are seeing strong attention after policy-linked inflows and lower borrowing costs.

However, every rally carries risk. Investors should not chase the longest duration or the highest yield without checking credit quality and liquidity.

The better strategy is disciplined reallocation. Keep emergency money safe, ladder maturities, prefer quality and use duration only where the time horizon supports it.

Frequently Asked Questions

Q. What are bond market yield curve adjustments?

They are changes in bond yields across different maturities, such as two-year, five-year and ten-year bonds.

Q. Why did short-end Indian bond yields fall recently?

Reuters reported that RBI-linked dollar-inflow measures encouraged buying in short and medium government bonds.

Q. Should investors move fully into long-duration funds?

No. Long-duration funds can rise when yields fall, but they can also fall sharply when yields rise.

Q. Are corporate bond funds safe after the rally?

They can be useful, but investors should check credit quality, issuer concentration and liquidity.

Q. What is a simple strategy for retail investors?

Use a laddered mix of liquid, short-duration and high-quality medium-duration exposure based on goals.